Business-to-business lending has become a lot more exciting in the past few years, moving from one-size-fits-all to being tailored to what businesses really need.

For daily operations we’ve seen the proliferation of Buy Now Pay Later and embedded finance options at checkouts, which give businesses the freedom to control their cash flow and make one off purchases without going into their overdraft.

For companies considering the next stage of growth, revenue based financing allows businesses to grow without giving away significant chunks of their company to investors, with different lending terms depending on the maturity of the business and what they need.

With all these lending models, the fundamental principal is the same: Give money out, get money back with some interest. What could be so hard?

Let’s get into the business model first

You have a big database of who your customers are, how much they owe, and what they’ve repaid. This means you know how much debt you’re liable for, what the repayment rates are, and if a loan gets extended you can just add it onto the customer’s record. Then once the debt is paid off you can mark that customer off and not worry about it any more. During the time of that customer’s relationship with you, you need to track the fees of servicing the debt and collections, plus your operating costs, then what’s left is the profits. Simple huh?

In reality a number of complexities creep in:

A mess of spreadsheets

Time to market is key, so instead of spending time getting up and running with a database and reconciliation built in, you start out using spreadsheets. This is fine, because why should you invest in tooling for payment ops at an early stage? You have a hacky, growth mindset! However, as your lending business is a success, you fly through seed, series A and then hit series B fundraising, only to realise your business is dependent on a web of spreadsheets and one persons knowledge of the web of integrations and macros running on top.

It goes without saying that tracking funds is essential so you know who is borrowing what and how much they have left against the original amount, and your teams shouldn’t be spending hours on manual reconciliation.

Not helped by a diverse payments stack

Direct debit is the most commonly used method to pay back borrowing. Although not every payment will fall into this path. Inevitably you have to provide a number of different payment methods to catch all the different issues that can arise. Bank transfers are always problematic, as you are not pulling the funds. Instead there are a multitude of human errors that mean you receive payments that take some detective work to reconcile.

It may be less than 5% payments that require manual reconciliation, but the proportion of time it takes your operations teams to then piece everything together is wildly disproportionate. Sorting and filtering different spreadsheets of extracted transaction data for references that won’t match is frustrating. Fees and erroneous payments involved in the process, so it’s not a straight 1-1 payback. It’s not worth the time constructing matching formulas in excel that doesn’t quite catch everything. Then once you’ve identified the corresponding payment, you have to get in touch with the customer to get the rest of your money.

Using software will automate the tracing of payments through from payment service provider to your bank account, so you no longer have to graft multiple data sources into a mega spreadsheets.

Product launches are slowed down by updating payments operations processes

Expanding into new territories and adding new product lines is great, however the additional complexities that come from new currencies, bank accounts or repayment flows should never be underestimated.

You have a choice to throw people, time or money at the problem. Ultimately your focus needs to be on what will make your customers happy and engaged, rather than building out backend tooling that strays from your core expertise.

If any of these problems sound familiar, do not fear, you’re not alone!

👉 Get in touch to see how Payable’s dashboard and APIs can make your team’s life easier

Announcements

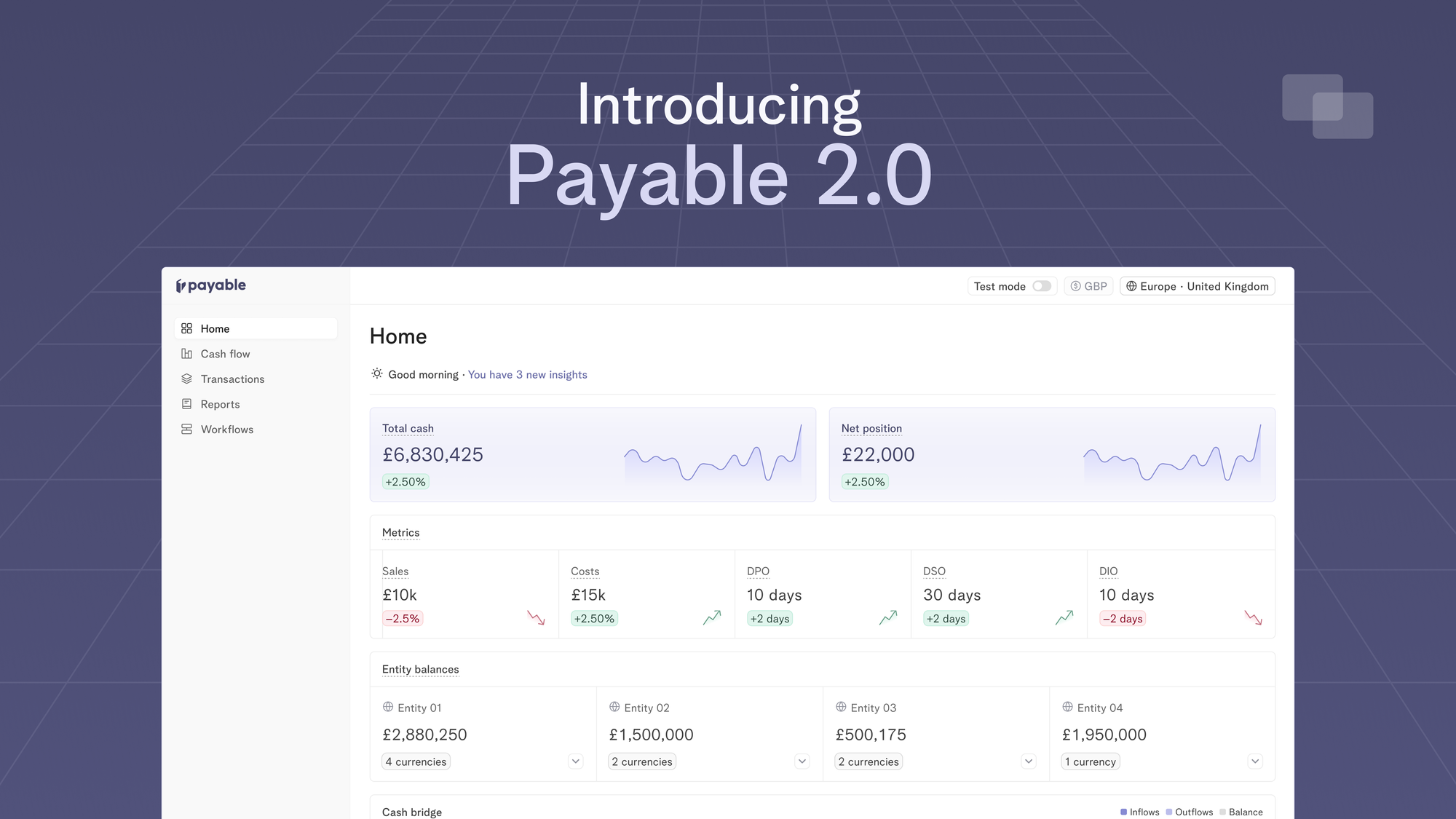

Introducing Payable 2.0 - one platform to optimise working capital, make fast liquidity decisions and move your cash metrics in real-time

13 Apr 2024

Today, we’re excited to launch Payable 2.0 which is our evolution to a more connected, intelligent and automated platform for finance teams to track their cash flows in real-time.

Cash Management

Mastering 13-week direct cash flow forecasts

26 Mar 2024

Knowing how your cash flow will behave in the future is crucial for the success and sustainability of any company. One way to achieve this is through the use of a 13-week direct cash flow forecast, which provides a detailed projection of a company's inflows and outflows over a specific time period.